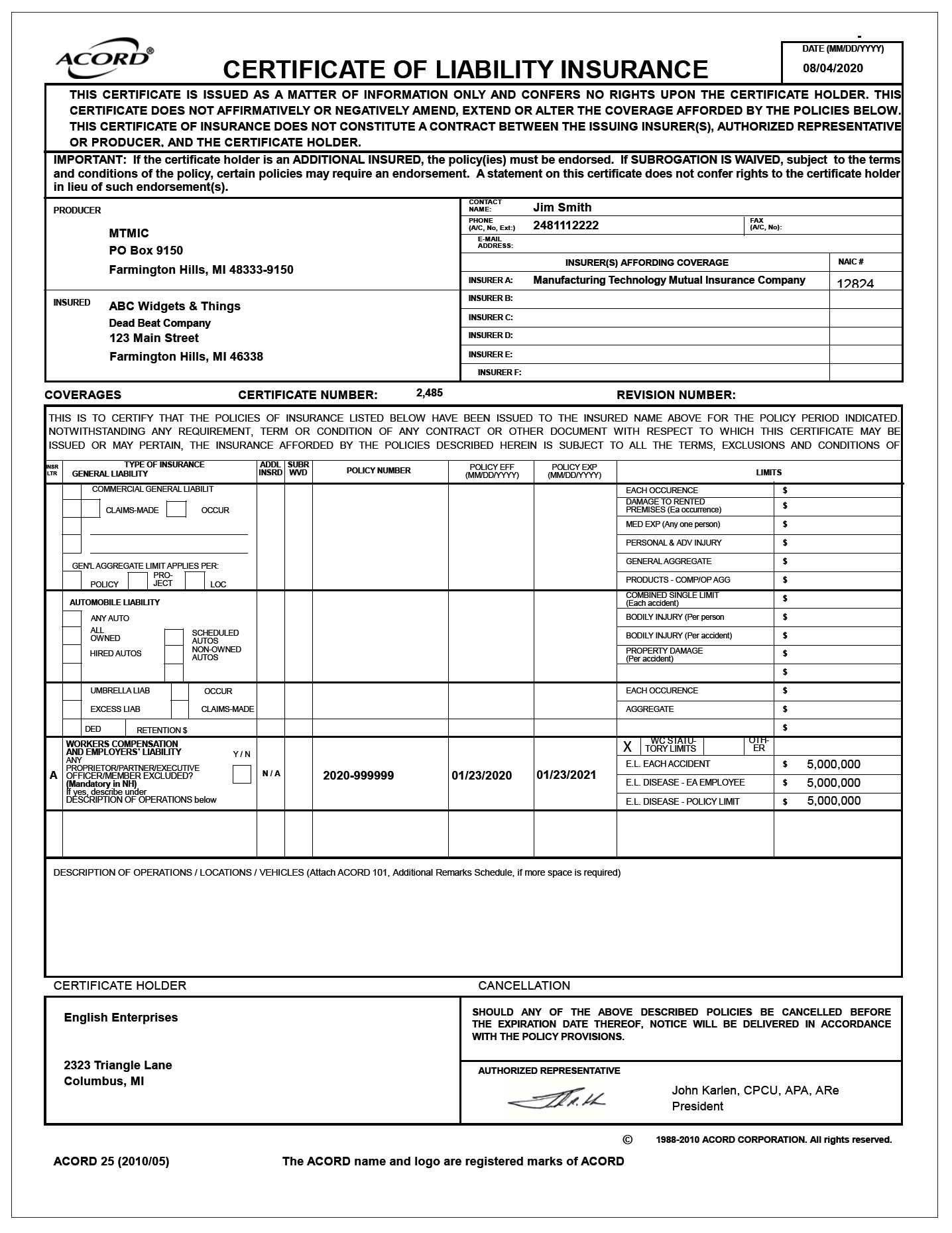

Certificate of Insurance

InsuranceA common request from our members is a Certificate of Insurance. Most often this is requested by a customer of our MTM member. That is a customer of our member is requesting that before they work at the customer’s location, the MTM member provides a Certificate of Insurance. For MTM members who work only at their own shop, a Certificate of Insurance rarely comes up. On the other hand, some of MTM members provide equipment maintenance/ repair/installation at their customer’s location, and this Certificate of Insurance is requested. There are two primary reasons that customers request this from our members.

- The MTM member’s customer wants to make sure that the company doing business at their location has their own insurance and is not relying upon the customer’s insurance to provide coverage.

- In workers’ compensation, if a subcontractor is not insured, the injured worker can then have their workers’ compensation benefits paid for by coverage at the work site, i.e. the customer’s insurance. So, the customer location wants to make sure they are not assuming workers’ compensation coverage and liabilities for workers that are not their employees.

The Certificate of Insurance is simple, costs MTM members nothing to get, and can most often be produced within a couple of hours of the request.

Additional Insured Endorsement

EndorsementAn Additional Insured Endorsement is sometimes requested by MTM members. This document provides that the MTM coverage extends to the customer. This is a standard request associated with general liability and property insurance coverage but with workers’ compensation insurance, this is an endorsement that causes difficulty. If MTM were to issue an Additional Insured Endorsement for your customer, a couple unintended consequences happen.

- If your customer was included as an additional insured on your workers’ compensation policy, all of their employees (and any of their injured employees) could then claim that your coverage applies to them. That you have assumed the customer’s workers’ compensation liabilities.

- The State keeps track of every employer and who their workers’ compensation insurance carrier is. If we provided an Additional Insured Endorsement, the State and courts would then believe that whoever you are working for is now part of your company and all their employees are your responsibility. The State would be raising this question because they would see duplicate coverage for one employer.

Because of these reasons, an Additional Insured Endorsement is not used for workers’ compensation coverage, however this is a common requested item for general liability and property coverages.You now have the basic rules of a Certificate of Insurance and an Additional Insured Endorsement. We would be happy to share more details to anyone that would like to know. Please call us and ask.